As we assess the damage that Trump and his friend Putin have lready done to American democracy, we need also to fight the damage they are trying to inflict on our economy and our people through Trumpcare. Read this:

It is a rare unifying moment. Hospitals, doctors, health insurers and some consumer groups, with few exceptions, are speaking with one voice and urging significant changes to the Republican health care legislation that passed the House on Thursday [May 4, 2017].

The bill's impact is wide-ranging, potentially affecting not only the millions who could lose coverage through deep cuts in Medicaid or no longer be able to afford to buy coverage in the state marketplaces. With states allowed to seek waivers from providing certain benefits, employers big and small could scale back what they pay for each year or reimpose lifetime limits on coverage. In particular, small businesses, some of which were strongly opposed to the Affordable Care Act, could be free to drop coverage with no penalty.

The prospect of millions of people unable to afford coverage led to an outcry from the health care industry as well as consumer groups. They found an uncommon ally in some insurers, who rely heavily on Medicaid and Medicare as mainstays of their business and hope the Senate will be more receptive to their concerns.

"The American Health Care Act [Trumpcare] needs important improvements to better protect low- and moderate-income families who rely on Medicaid or buy their own coverage," Marilyn B. Tavenner, the chief executive of America's Health Insurance Plans, the industry's trade group, said in a strongly worded statement.

Others were even more direct about the effects the bill would have, not only on patients but also on the industry. "To me, this is not a reform," said Michael J. Dowling, the chief executive of Northwell Health, a large health system in New York. "This is just a debacle."

"Hospitals that serve low-income patients "will just be drowning completely when this happens," Mr. Dowling said, noting that more people would become uninsured at the same time that government payments to cover their costs were reduced.

In contrast to hospital and doctor groups, insurers had largely remained silent about their reservations, perhaps in the hopes of bartering their low profile in exchange for assurances that billions of dollars in subsidies for low-income coverage would continue. The White House and Congress have gone back and forth about their willingness to pay for the subsidies, prompting anxiety among some companies. Several, including Anthem, have threatened to sharply raise their prices or leave markets altogether without the funding.

But a few, including Blue Shield of California, came out in opposition to the bill before the vote. "We feel compelled to oppose it," said Paul Markovich, the company's chief executive. "It raises the specter that the sickest and neediest among us will be disproportionately hit in losing access."

After the House passed the bill on Thursday, the industry's two major trade groups urged lawmakers to increase the tax credits available to help people pay for coverage, and to adjust them to assist those who are older, live in high-cost areas or have lower incomes.

But the overriding concern — for insurers, many workers and officials throughout the health care systems in many states — is the broad reductions proposed for Medicaid. Even for insurers that have largely abandoned the individual market, like UnitedHealth Group and Aetna, a substantial portion of their business is providing coverage under Medicaid [which will be cut by $880 billion which is 25% of the existing program].The same is true for many local nonprofit plans, said Ceci Connolly, the chief executive of the Alliance of Community Health Plans.

Employers and others said they were also concerned about the effects on freelancers, who do not have a traditional employer but are self-employed or contract workers in the so-called gig economy.

Depending on their income, those workers have shuttled between Medicaid and the individual insurance market under the federal health care law, which offered a greater level of stability, said Nell Abernathy, vice president for research and policy at the Roosevelt Institute, a left-leaning economic research organization.

"A huge swath of Americans are in insecure work arrangements," she said. "This repeals that level of security, which was not perfect, but it was a step in the right direction."

Small businesses, which were sharply divided over the original law, remained mixed in their response to the Republican bill, and there seemed little doubt that some companies would drop coverage in the absence of any penalty. The National Federation of Independent Business, which opposed the Affordable Care Act, said the House legislation was "a crucial first step toward health care reform.

"In other people's view, employees of small businesses would lose out if Medicaid were rolled back or the exchanges became threadbare, because many smaller companies rely on employees' ability to obtain coverage through the government program or individual market."

The Main Street Alliance, a group of small-business owners that supported the Affordable Care Act, said four million small-business owners, employees and self-employed entrepreneurs had gained insurance under the law, and that an additional six million small-business workers had signed up for Medicaid through the law's expansion.

"This bill leaves small-business owners in a terrible position, one they were all too familiar with before the A.C.A.: unable to afford premium hikes year to year, unsure their employees will be healthy and able to work, and uncertain of the future of their businesses," said Amanda Ballantyne, national director of the Main Street Alliance.

The recent amendments to the bill also raised questions about coverage for people with pre-existing medical conditions, which has become an emotional flash point for opposition. The bill would allow states to waive some of the current rules banning insurers from charging sick people more or excluding certain benefits, and those waivers could have broad effects if employers are no longer required to provide comprehensive coverage. Before the Affordable Care Act, many employers capped how much they would pay for care over a person's lifetime at $2 million, said Tracy Watts, a senior partner at Mercer, a benefits consultant.

While it is unclear what states would allow under a waiver or when such waivers would go into effect, employers could revisit the limits and drop types of benefits if a state deemed them nonessential.

A January survey of 666 employers by Willis Towers Watson, a benefits consultant, found that while many employers planned to keep most of the mandatory benefits, a significant minority were already mulling changes. While half indicated that they were unlikely to reinstate lifetime limits, 15 percent said they would consider doing that.

And employer groups generally favored provisions of the bill that would reduce taxes, particularly the so-called Cadillac tax on high-cost health plans, which was delayed for several years. Employers favor its overall repeal.

Some health care groups, like medical device manufacturers, supported the bill because of specific provisions like the repeal of a 2.3 percent device tax under the Affordable Care Act. That tax was suspended for two years in 2015, but the industry wants a permanent repeal. The Pharmaceutical Research and Manufacturers of America, the drug industry's largest trade group, said it had not taken a position on the bill.

Unlike doctors and hospitals, which would most likely experience an immediate hit if millions of Americans lost insurance, medical device manufacturers and the drug industry would probably feel a more muted effect. The drug industry, for example, might sell fewer products and lose revenue.

"Fewer patients are treated, so it's bad for them, but it's a lot worse for hospitals and the impact on physicians," said Ronny Gal, an analyst for Bernstein who covers the drug industry. "They're a little bit on the tail end of this."

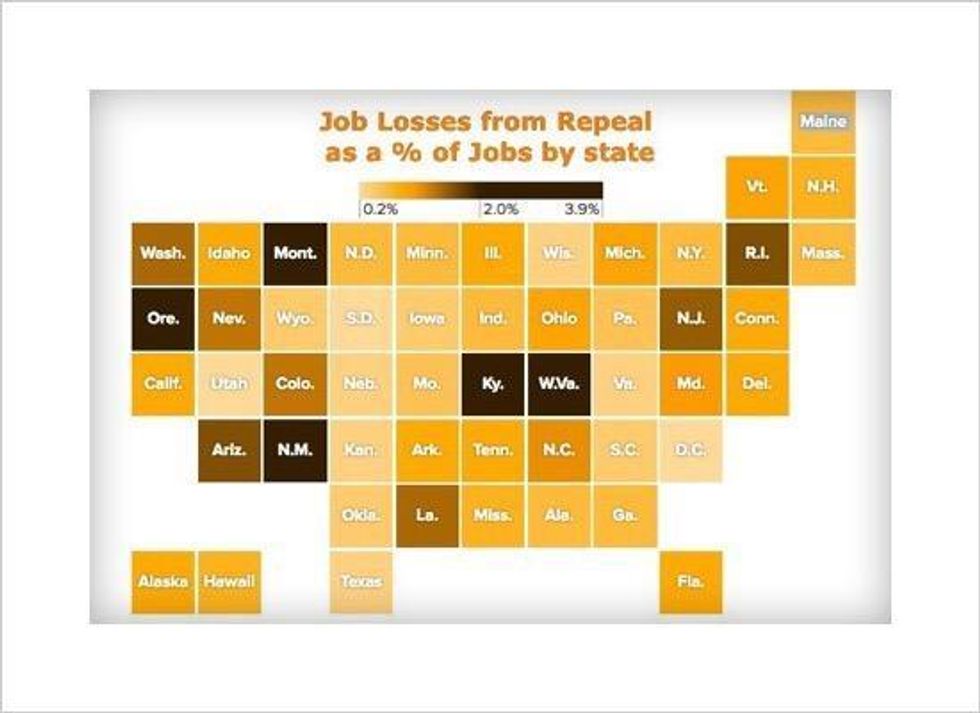

This article by Reed Abelson and Katie Thomas was published in the New York Times as Hospitals, Doctors and Insurers Criticize Health Bill on May 6, 2017. The follow up was Health Act repeal could threaten U.S. Job Engine.

That article suggests Obacare repeal would cost the economy 1 in 8 jobs.

Today these additional words appear in The Times, this time on the effect of Trumpcare on employee provided healthcare.

If it becomes law, the American Health Care Act will have the biggest effects on people who buy their own insurance or get coverage through Medicaid. But it also means changes for the far larger employer health system.

About half of all Americans get health coverage through work. The bill would make it easier for employers to increase the amount that employees could be asked to pay in premiums, or to stop offering coverage entirely. It also has the potential to weaken rules against capping worker's benefits or limiting how much employees can be asked to pay in deductibles or co-payments.

However you get your insurance (and we hope you have it), this bill will affect you badly, unless you are mega-rich and will get a tax cut.

Tell your Senators. 202-324-3121.

###

May 9, 2017